[1]:

import matplotlib.pyplot as plt

import yaml

import numpy as np

from ruspy.simulation.simulation import simulate

from ruspy.model_code.fix_point_alg import calc_fixp

from ruspy.model_code.cost_functions import lin_cost

from ruspy.model_code.cost_functions import calc_obs_costs

from ruspy.estimation.estimation_transitions import create_transition_matrix

Simulation tutorial

This notebook provides a tutorial of how to use ruspy’s simulation function simulate. Furthermore, the convergence of expected utility calculated by fixed point algorithm and the observed utility on the simulated data are demonstrated.

First we specify the initialization dictionairy for the simulation.

[2]:

# Set simulating variables

disc_fac = 0.9999

num_buses = 100

num_periods = 80000

gridsize = 1000

# We use the cost parameters and transition probabilities from the replication

params = np.array([10.07780762, 2.29417622])

trans_probs = np.array([0.39189182, 0.59529371, 0.01281447])

scale = 1e-3

init_dict = {

"simulation": {

"discount_factor": disc_fac,

"periods": num_periods,

"seed": 123,

"buses": num_buses,

},

"plot": {"gridsize": gridsize},

}

Beside the initializsation dictionary, the simulate function takes other inputs. These objects are calculated below and are passed to the simulation function, which returns the simulated data.

[3]:

# Calculate objects necessary for the simulation process. See documentation for details.

num_states = 200

costs = calc_obs_costs(num_states, lin_cost, params, scale)

trans_mat = create_transition_matrix(num_states, trans_probs)

ev = calc_fixp(trans_mat, costs, disc_fac)[0]

[4]:

# Simulate the data.

df = simulate(init_dict["simulation"], ev, costs, trans_mat)

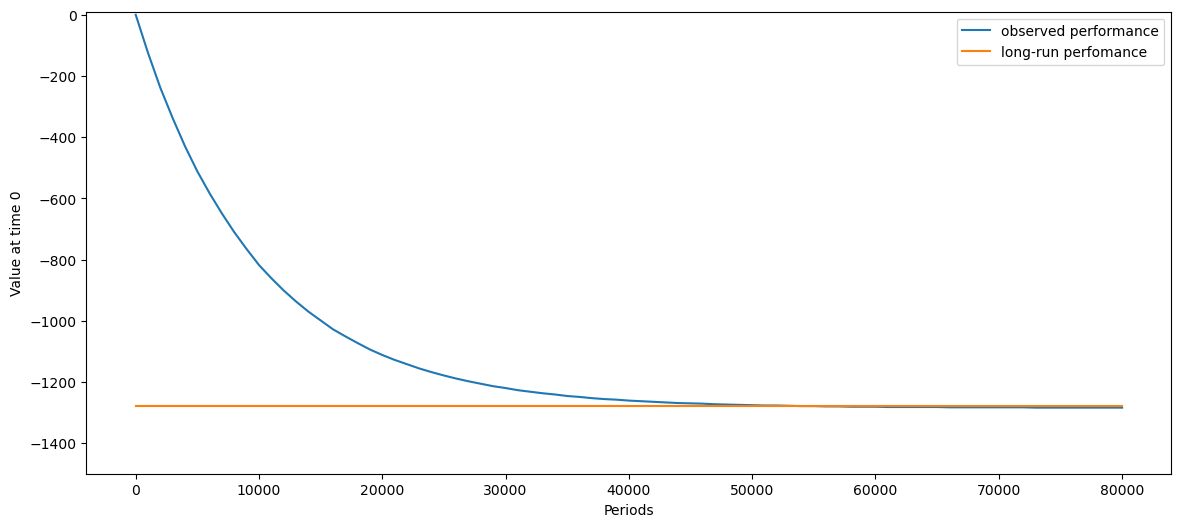

In the following, a exercise is provided, which shows the convergence of expected utility calculated by fixed point algorithm and the observed utility on the simulated data.

[5]:

# Provide a discounting function.

def discount_utility(df, disc_fac):

v = ((disc_fac ** df.index.get_level_values("period")) * df["utilities"]).sum()

return v / df.index.get_level_values("Bus_ID").nunique()

[6]:

# Discount the utility of the observed data

num_points = int(num_periods / gridsize) + 1

periods = np.arange(0, num_periods + gridsize, gridsize)

v_disc = np.zeros_like(periods)

for i, period in enumerate(periods[1:]):

v_disc[i + 1] = discount_utility(df[df.index.get_level_values("period") <= period], disc_fac)

[7]:

# Create an array containing the expected long-run performance.

v_exp = np.full(num_points, ev[0])

The results are now visualized in oder to show convergence of the observed utility on the simulated data to the expected utility by the fixed point algorithm.

[8]:

fig, ax = plt.subplots(figsize=(14, 6))

ax.set_ylim([-1500, 10])

ax.set_ylabel(r"Value at time 0")

ax.set_xlabel(r"Periods")

ax.plot(periods, v_disc, color="#1f77b4", label="observed performance")

ax.plot(periods, v_exp, color="#ff7f0e", label="long-run perfomance")

ax.legend()

[8]:

<matplotlib.legend.Legend at 0x7fce11936b20>